Delaware vs Ireland for AI Companies: Which Structure Works Better for EU Market Access?

Delaware vs Ireland for AI Companies:

Which Structure Works Better for EU Market Access?

Delaware gives you US VC. Ireland gives you EU AI Act compliance, the Knowledge Box, and GDPR by default. For many AI companies the answer is both — but the structure depends on where you are raising and where your users are.

The Delaware vs Ireland question comes up at a specific moment: when a US-funded AI company realises its product is being used by EU customers, or when a European AI company receives its first US term sheet and is told to “flip to Delaware.” At that point, the two jurisdictions are not alternatives — they may both be required, structured around each other.

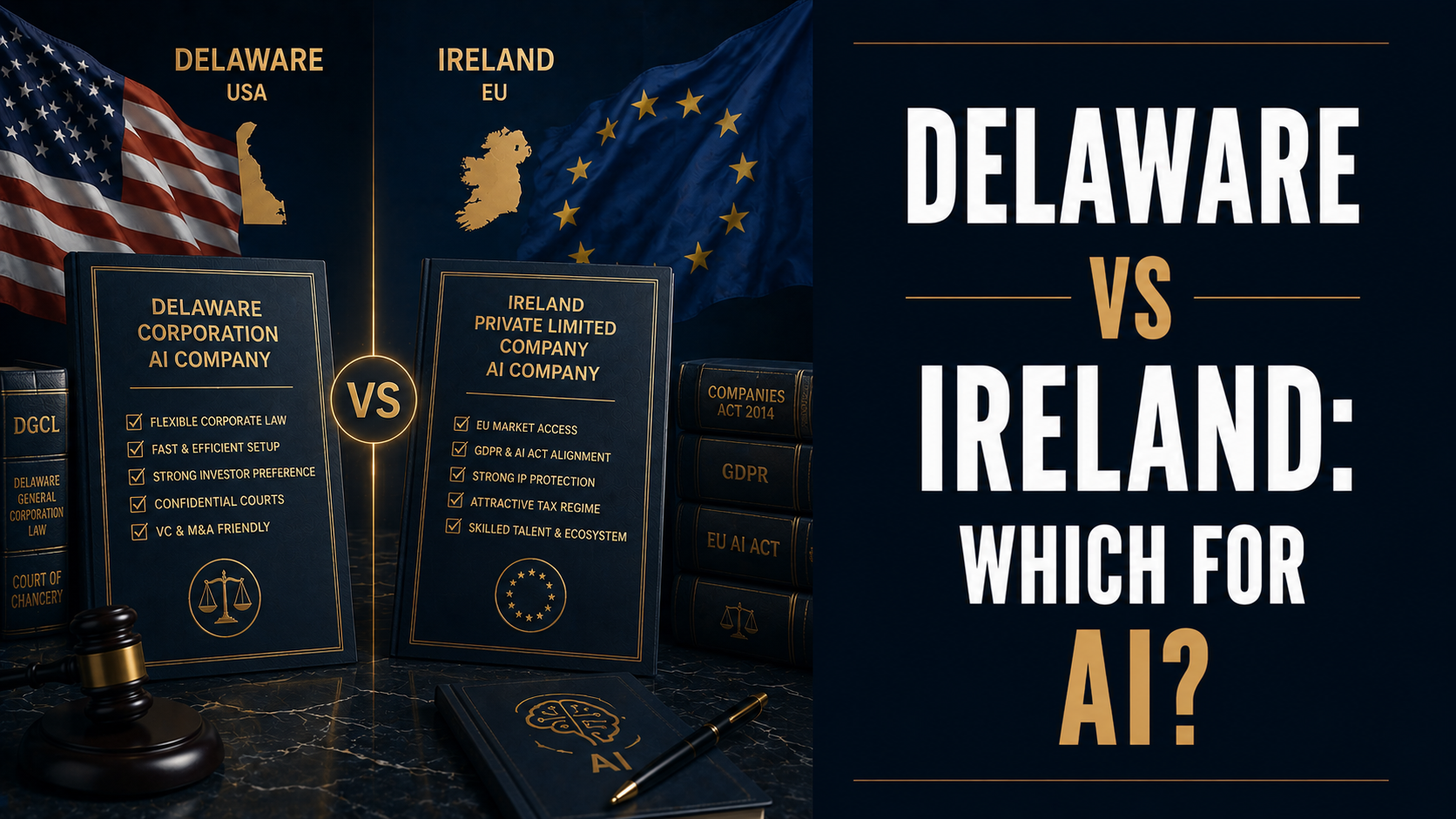

The comparison matters because Delaware and Ireland optimise for different things. Delaware is the global standard for US VC-compatible equity structures. Ireland is the leading EU choice for AI companies that want EU AI Act compliance by default, Ireland’s Knowledge Development Box on IP income, and a common-law entity familiar to enterprise customers across Europe. Understanding exactly what each gives — and what each costs — is the first step to choosing correctly.

Our AI jurisdiction structuring practice advises AI companies on single-entity and dual-entity structures, IP holding arrangements, and the intercompany agreements needed to connect Delaware and Irish entities effectively.

Delaware vs Ireland — Seven Parameters

A direct comparison across the parameters that matter most for AI companies. Each cell shows the assessment for each jurisdiction, with a badge indicating whether this parameter is an advantage, neutral, or a consideration requiring attention.

Which Structure for Your AI Company? Decision Tree

Answer three questions to get a structure recommendation and the key next steps for your situation.

Pre-Decision Checklist: What to Resolve Before You File

Eight questions to work through before committing to a Delaware or Irish entity. Changing the answer to any of them after incorporation is expensive. Click each item to track completion.

The answer depends on your investor profile and EU market plans. Delaware is better if you are raising from US institutional VCs and your primary market is North America — it is the required structure for standard NVCA investment documents and gives you maximum flexibility for a US exit or IPO. Ireland is better if you are raising from EU VCs, your product will have significant EU users, and you want EU AI Act compliance by default together with Ireland’s Knowledge Development Box (effective 6.25% rate on qualifying IP income).

For companies targeting both US capital and EU markets, neither Delaware nor Ireland alone is the optimal answer. The dual structure — Delaware parent with Irish subsidiary — is designed precisely for this scenario. The additional administrative overhead (typically EUR 15,000–30,000 annually) is justified once EU revenue and IP licensing income reach a scale where the KDB savings exceed the cost.

Yes, but with additional legal work and sometimes additional time. US VCs strongly prefer Delaware C-Corps and many fund LPAs restrict direct investment into non-US entities without additional approval or legal structuring. An Irish company can receive US VC investment, but the fund’s legal team will typically require a flip — a redomiciliation of the Irish company into a Delaware C-Corp — before the round closes. This flip is a real transaction with legal costs (typically USD 20,000–40,000) and takes four to eight weeks.

US VCs with established EU portfolios — particularly those with Dublin offices or existing Irish portfolio companies — are more comfortable investing directly into Irish entities and will sometimes do so without requiring a flip. For a company planning to raise from both US and EU VCs, the dual-entity structure (Delaware parent, Irish subsidiary) from inception avoids the flip and gives both investor types a familiar entity to invest into.

Ireland’s Knowledge Development Box (KDB) reduces the effective corporate tax rate on income derived from qualifying intellectual property to 6.25% — compared to the standard 12.5% Irish corporate rate and the US federal rate of 21%. The KDB applies to income from patented inventions and certain other qualifying assets where the IP was developed through R&D activity in Ireland (the OECD nexus approach requires the R&D and the IP to be linked).

For AI companies, qualifying income under the KDB can include: royalties from licensing patented AI systems; trading income directly from exploitation of qualifying IP; and income from the sale of qualifying assets. In addition to the KDB, Ireland offers a 25% R&D tax credit on qualifying expenditure — refundable in some cases — which is immediately valuable for AI companies investing in model development, training infrastructure, and evaluation. The combination of KDB and R&D credit is the strongest IP tax incentive regime in the EU for AI companies with real R&D activity in Ireland.

Yes, if the Delaware company deploys AI systems used by EU-based users. Article 22 of the EU AI Act requires non-EU providers to designate an EU-authorised representative — an entity established in an EU member state that is mandated in writing to act on behalf of the provider. The representative must be identifiable, must register in the EU AI database for high-risk systems, and serves as the contact point for EU national supervisory authorities.

The Article 22 representative satisfies the regulatory compliance requirement but is not a full EU legal entity. It does not give you a local contracting counterparty for EU enterprise customers, does not satisfy GDPR establishment requirements for EU data processing, and does not provide access to EU public procurement. For AI companies with significant EU B2B revenue, a full Irish subsidiary is almost always the better long-term choice — the representative is a lighter-touch option for companies with limited EU exposure at early stage. See our detailed analysis of how the EU AI Act applies to non-EU providers.

The dual structure has a Delaware C-Corp as the parent entity (holding all the equity, issuing stock options to founders and employees under US-standard plans, receiving investment from US and international VCs under NVCA-compatible documents) and an Irish limited company as the EU operating subsidiary (owned 100% by the Delaware parent, holding EU IP, employing EU team members, contracting with EU customers, and satisfying EU AI Act obligations as an EU-established provider).

The two entities are connected by: (a) an intercompany services agreement under which the Irish subsidiary provides development services to the Delaware parent; and/or (b) an IP licensing agreement under which the Irish entity licenses AI model IP to the Delaware entity for use outside the EU, generating KDB-eligible royalty income for the Irish entity. Transfer pricing documentation is required to ensure the intercompany pricing is arm’s-length. Both entities need annual audits and corporate governance. The real-world cost of maintaining this structure — additional legal, accounting, transfer pricing compliance, and director fees — is typically EUR 15,000–30,000 annually above what a single-entity company would spend. This overhead is justified at Series A scale and above, but is usually premature for pre-seed companies.

Delaware gives you US VC.

Ireland gives you Europe.

The structure gives you both.

WCR Legal advises AI companies on the Delaware + Ireland dual structure — from entity formation and IP transfer to intercompany agreements, transfer pricing, and EU AI Act compliance. We build structures that work for US and EU investors simultaneously.

Post Comment