Double Company Structure for AI Startups: Holding in Ireland or Netherlands, Operations in Estonia

Double Company Structure for AI Startups:

Holding in Ireland or Netherlands, Operations in Estonia

Two entities, two jurisdictions, one purpose: hold the AI IP where it gets the best tax treatment, operate where costs are lowest and the EU AI Act applies by default. Here is how the structure works and how to build it correctly.

The double company structure is one of the most widely discussed legal architectures for AI startups — and one of the most poorly understood. Founders hear about it from investors or other founders, often in the form “you need a holding company in Ireland for the IP,” without a clear explanation of what this means, how it works, or when it is actually the right structure to implement.

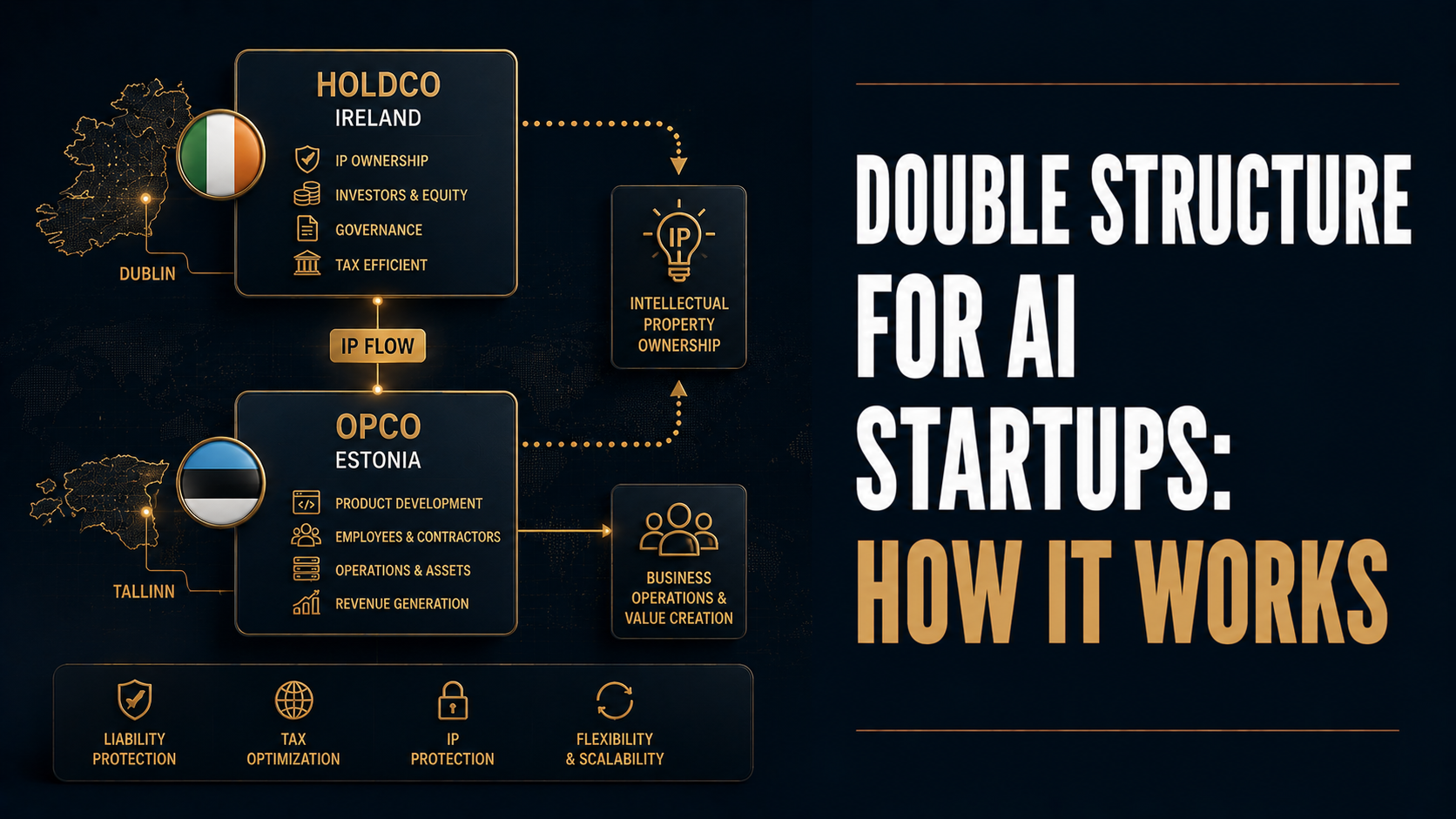

At its core, the structure separates two distinct functions: IP ownership (HoldCo — holds model weights, training data rights, patents, and methods) and operations (OpCo — builds the product, employs the team, contracts with customers, and satisfies regulatory obligations). The HoldCo licenses IP to the OpCo on commercial terms, generating royalty income taxed at a preferential IP box rate. The OpCo deducts the royalty payment, reducing its taxable operating profit.

The most common configuration for EU-focused AI startups is an Irish HoldCo (Knowledge Development Box: 6.25% effective rate) or Dutch HoldCo (Innovation Box: 9% effective rate), with an Estonian OÜ as the operating entity. Our AI jurisdiction structuring practice builds and documents these structures from entity formation through transfer pricing.

Why the Double Structure Emerged for AI Startups

The double company structure is not a new invention for AI — it has been used in technology and pharmaceutical IP for decades. But AI changes the economics in four specific ways that make it more valuable for early-stage companies than it was for earlier software businesses.

Ireland HoldCo vs Netherlands HoldCo — Seven Parameters

Both Ireland and the Netherlands offer well-established IP holding environments with preferential IP box regimes. The differences matter for AI companies at different stages and with different capital structures.

Interactive Structure Diagram — Three HoldCo Options

Select a HoldCo jurisdiction to see the full two-entity structure, the intercompany flows, and the key advantages and considerations for each configuration.

Build Steps Checklist: How to Set Up a Double Structure

Nine practical steps for building a correctly structured HoldCo + OpCo arrangement. Work through these in order — the sequence matters. Click each item to track completion.

A double company structure involves two separate legal entities: a holding company (HoldCo) that owns the intellectual property — model weights, training data rights, patents, and AI methods — and an operating company (OpCo) that runs product development, employs the team, contracts with customers, and interfaces with regulators including the EU AI Act.

The HoldCo licences its IP to the OpCo under an intercompany agreement, generating royalty income taxed at the HoldCo’s IP box rate (6.25% in Ireland, 9% in the Netherlands). The OpCo deducts the royalty payment as a business expense. The most common configuration for EU AI startups is an Irish or Dutch HoldCo combined with an Estonian OÜ operating entity. See our full article on intra-group AI IP licensing and royalties →

Estonia is commonly used as the EU operating entity for three reasons. First, it is an EU member state — the operating company satisfies EU AI Act establishment requirements by default, with no separate representative needed. Second, Estonia’s e-Residency programme allows founders to manage the company digitally without physical presence, which is cost-effective for distributed teams. Third, Estonia’s 0% corporate tax on undistributed profits means operating profits can accumulate and be reinvested without immediate tax drag.

The OpCo’s royalty payments to the HoldCo are deductible expenses under Estonian tax law, which further reduces the effective tax on operating income. The combination — low setup cost, digital-first management, EU entity status, and 0% retained earnings tax — makes Estonia the most efficient EU operating entity for AI companies that hold their IP in a higher-substance, higher-benefit HoldCo jurisdiction.

Ireland offers a lower IP box rate (6.25% KDB vs 9% Dutch Innovation Box) and a common law legal system familiar to US counsel, with no notarisation requirement for incorporation. Ireland is the better choice for: AI companies with patentable IP (core AI methods); companies raising from EU or US VCs; and companies where the KDB rate differential justifies the patent filing cost.

Netherlands offers more flexible IP qualification (R&D certification without formal patent may be sufficient) and a more established treaty network for dividend flows in complex multi-entity structures. Netherlands is better for: companies whose AI IP does not meet Irish patent requirements; post-Series A structures with complex US-EU holding layers; and companies with existing Dutch investors or Dutch-domiciled parent entities. For most pre-Series A AI startups, Ireland is the more accessible and cost-effective HoldCo choice.

The HoldCo grants the OpCo a licence to use the AI IP assets — model weights, training data, methods, patents — in exchange for a royalty payment. The royalty rate must reflect what an independent party would pay for equivalent IP access (the arm’s-length standard under the OECD Transfer Pricing Guidelines). A transfer pricing study must document and justify the rate.

The OpCo deducts the royalty payment as a business expense, reducing its taxable profit. The HoldCo receives the royalty as income, taxed at the KDB rate (6.25% in Ireland). The economic benefit is the difference between the rate that would otherwise apply to this income and the IP box rate. For more detail, see our analysis of intra-group AI IP licensing and royalties.

A double structure is premature when the administrative overhead exceeds the tax benefit. The annual cost of maintaining two entities typically runs EUR 15,000–30,000 above a single-entity structure (dual audit, transfer pricing documentation, intercompany invoicing, dual corporate governance). This overhead is only justified when IP licensing income is material enough that the IP box rate difference creates real savings, or when investors require the dual structure as a condition of investment.

For pre-revenue and early-revenue AI startups, a single Estonian entity is usually the better starting point — low cost, EU entity status, EU AI Act compliance, and 0% retained earnings tax. The HoldCo + OpCo structure should be built when the company reaches the scale where the KDB savings clearly exceed the structural overhead — typically at or shortly before Series A, when IP licensing income or EU enterprise revenue reaches a level that justifies the complexity.

Hold the IP where it earns most.

Operate where friction is lowest.

WCR Legal builds and documents double company structures for AI startups — entity formation, IP transfer agreements, intercompany IP licences, transfer pricing documentation, and EU AI Act registration for the Estonian OpCo.

Post Comment